Inflation is Up, Unemployment is Down

So What Happens to My Portfolio?

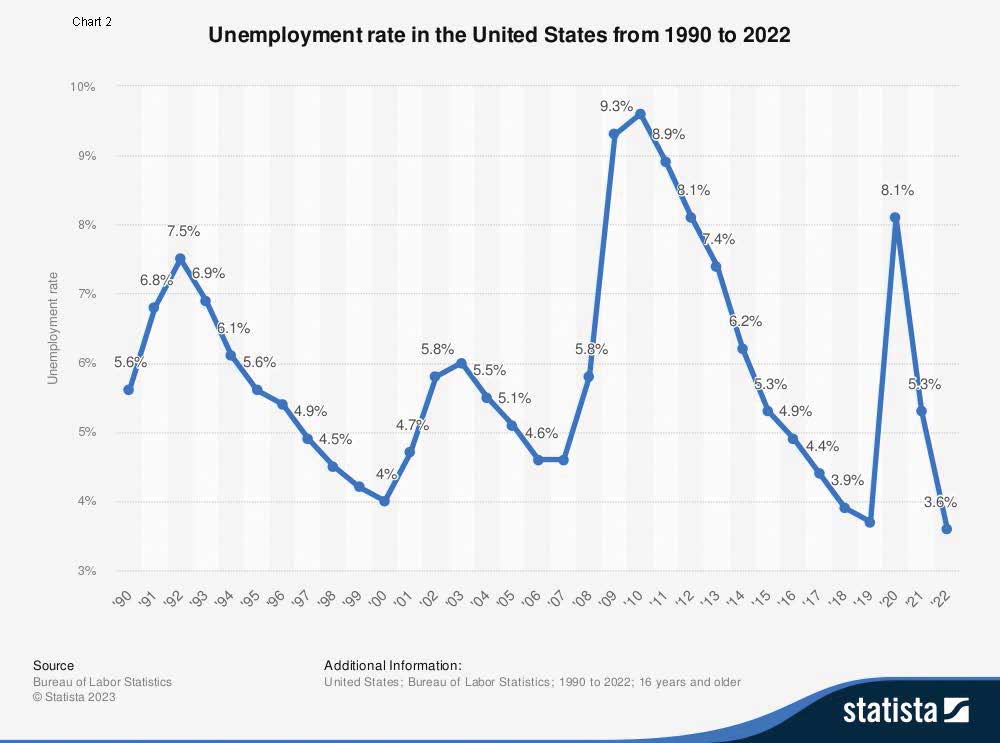

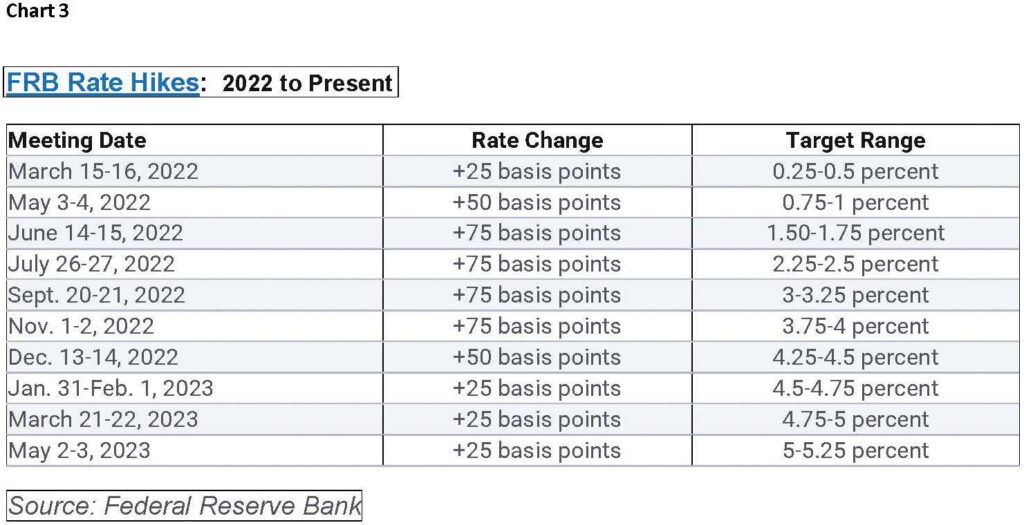

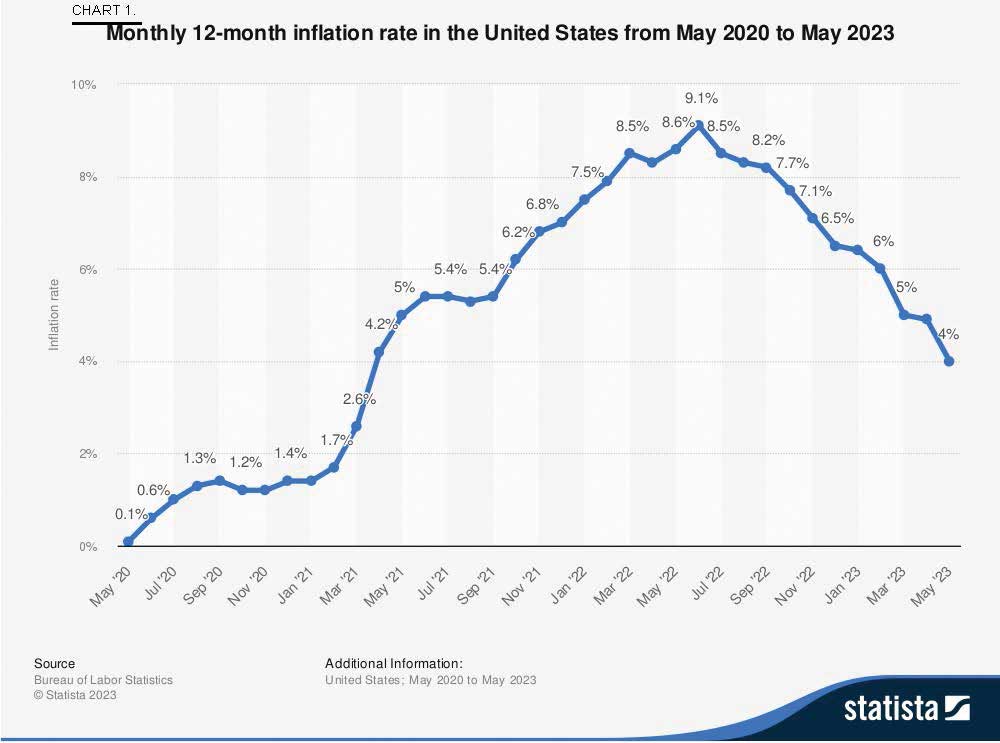

After many quiet years, inflation roared back after the Pandemic. The US annualized CPI rose from 1.7% in March, 2021 to 9.1% in June, 2022 (see Chart 1). The Federal Reserve raised interest rates by 500 basis points over the past 15 months (see Chart 3). As a result, the CPI eased to 4% by May 2023, but that is still twice the Fed’s 2% Annual CPI target. Meanwhile, historically high employment (see Chart 2) is creating additional inflationary pressure on wages and disrupting labor flows.

Resorts face multiple economic challenges today: reduced purchasing power, rising wages, higher interest rates, and tighter credit. Loan and maintenance fee receivables remain the key to overcoming these challenges. Whether our clients are borrowing on their portfolios, securitizing them, selling them, originating new sales, or just trying to maximize collections and recoveries on seasoned accounts – receivables remain the lifeblood of our industry. We are frequently asked what are the impacts of inflation on loan and maintenance fee receivables, and how can portfolio managers mitigate risks and leverage opportunities in this economic cycle?

The answers vary. A rising tide can float all the boats, or it can destroy the harbor. Here are some factors to consider:

• Are you a developer, a management company, vacation club, HOA, or a hybrid of these?

• What is the leverage on your receivables?

• What is the average FICO © and Seasoning on your receivables?

• Have you quantified your customers’ average ‘paid-in equity’ and ‘value proposition’?

• How and where are your portfolios serviced and collected?

• Is your resort still in sales or marketing mode?

• How do you deploy vacant inventory and significant amenities?

For readers who manage both loans and maintenance fees, we suggest an integrated ‘whole customer’ approach. Accountants, financiers and regulators may require that loans be presented differently than maintenance fees on your balance sheet. But consumers don’t care about your balance sheet. They are just focused on their pocketbook, and all the bills they have to pay in order to use their vacation. However, for simplification we have analyzed the two types of receivables separately.

Loans:

In the past, developers and vacation clubs hypothecating, securitizing or selling their loan portfolios enjoyed a big ‘spread’ between the low variable interest rates charged by Lenders (or the low yield required by Investors) versus the high fixed interest rates they charge consumers. That spread shrunk considerably over the past 15 months, as the Fed raised interest rates to temper inflation, and Lender and Investor interest rates climbed commensurately. Bill Ryczek, a VOI industry veteran and Senior Partner at Colebrook Financial, LLC, summarized this situation for us. “One of the most significant factors affecting our developer clients is the increase in interest rates, which causes more of the monthly collections from their receivable portfolios to be applied to interest and less to principal. That makes it more difficult to accumulate equity in a portfolio, which is often a source of liquidity. The rate charged to consumers is generally static and doesn’t move with changes in rates. Therefore, arbitrage income is being squeezed and the amount of equity a developer will eventually realize from the portfolio is diminished.”

Related: Resort Tips for Battling Rising Costs of Inflation

Interest rate protection can mitigate this problem. We have helped several clients sort out the costs and benefits of caps, collars, swaps, buying a fixed rate, and other hedging tools. Also, where permitted by law, developers can increase interest rates on new consumer loan originations, boosting the yield on their portfolios and regaining some arbitrage. Notably, there are jurisdictions where variable-rate consumer timeshare financing is permitted; however, we have seen that backfire, and recommend against it.

As disruptive as inflation is for many resorts, it is downright scary for consumers. This creates a sales and marketing opportunity. Josh Herschlag, a marketing executive for 35+ years with Shawnee, Rank PLC, and Resorts Group, Inc. who now consults with Fairshare Solutions, points out, “One of the value propositions in Timeshare sales is that it allows consumers to lock in today’s prices and not have to worry about rising accommodation costs in the future.”

Josh also reminds us, “For existing Timeshare owners, higher inflation rates can make the perceived value of their Timeshare greater and may have a positive impact on their propensity to make payments.” This is true for established obligors, and those with higher income and credit scores. However, consumers with moderate income are often the first to be pinched by inflation, and cut back on discretionary spending. Over the past 15 months, we have seen increased delinquency on portfolios with FICO © scores under 675, or paid-in equity under 25%, or seasoning under 24 payments.

We believe that this trend of increased delinquency will continue until the annualized CPI is below 3%, even if we avoid the mild recession predicted by many economists. Accordingly, we recommend protecting your receivables by refocusing on value delivered to the consumer. Make sure that servicing, collections, reservations, exchange, and customer service all work together to maximize usage and enjoyment. Wherever possible, get paying consumers on vacation, and ensure that customers who cure delinquency get immediate access to travel and benefits. Be mindful that strategies like bonus weeks, discounted rentals, amenity passes, and enhancing exchanges with developer points, can be marginally accretive while also reducing portfolio delinquency.

Use social media, e-communication, and direct mail to target ‘marginal’ portfolios without any overt reference to the customers’ accounts. Simply maximizing satisfaction and value for consumers whom you identify as at risk for increased delinquency will improve collections. The present environment is also ideal for incentivizing consumers to go on ACH, which will significantly improve delinquency and lower servicing costs. All of foregoing are ‘carrots’, here is one ‘stick’: If you or your service bureau are not auto-reporting consumer payments to credit bureaus, consider doing so. We recommend notifying your customers 60 days in advance – you will see an uptick in currency and cash flow.

Maintenance Fees:

A lot of older resorts already faced declining membership and aging facilities before the inflationary spiral of the past 15 months. Additionally, wage inflation for housekeepers, janitorial and service staff has actually exceeded the increase in CPI. Most resorts have passed such financial burdens directly to their members, in the form of sharply higher maintenance fees. As a result, maintenance fee delinquency has spiked among many of the management companies and HOAs seeking our help. We believe that this trend will continue even after inflation is back under control, unless some significant changes are implemented.

Again, we recommend mitigating delinquency by refocusing on value delivered to the consumer. There are different opportunities to do this at older ‘legacy’ resorts no longer under developer control. Look for novel ways to monetize vacant inventory and underutilized amenities. Where feasible, add value via outside travel and exchange. Where appropriate, leverage paying maintenance fees via short-term hypothecations, or reach out to current obligors with offers of enhanced usage or reservations in return for pre-payment.

Related: Inflation Busters: Protecting Profits as Costs Rise

Make sure that billing and collections are handled by a company that supports and understands timesharing. Where feasible, facilitate travel and exchange for paying members, and insist that your collection agency do so in a robust way for members who reinstate. Empty inventory can be monetized in many ways, even if it has not been reconveyed, including: OTA rentals, member rentals, granting additional usage to current members, and moving reservations for good-payers to larger units or more desirable time.

If you have extra acreage at your resort, consider a passive JV with an amenity provider. Andy Worthington, President of TreeCourseAdventures, LLC, suggests, “Many older resorts have great locations and lots of members, but lack capital or expertise to construct an amenity. Consider leasing the site to a reputable operator who builds and runs an amenity. This can generate significant new bottom-line revenue for your resort, without operational headaches. And insist that your members and guests have deeply discounted amenity usage. That increases member satisfaction, resort reservations, and ADR.”

Offer consumers the option to go on monthly EFT or ACH, instead of annual billing. Some members prefer spreading out their maintenance fee payments, while your resort is effectively pre-paid instead of waiting for an annual lump sum. The potential improvement in cash flow justifies incentivizing this option where needed.

Harry Van Sciver is the President of Whitebriar Financial Corporation (www.whitebriar.com) and Director of Fairshare Solutions (www.fairshare.solutions). He has a lifetime of experience in resorts, banking, finance, and collections. Harry is also a Director of Resorts Group, Inc.

Dennis Rogers is the President of Fairshare Solutions, LLC (www.fairshare.solutions). He has spent 35+ years running Portfolios, Servicing, and Collections for major developers and finance companies.