2020 Report to the Nations: Insights and Lessons on Occupational Fraud

In 2020, the Association of Certified Fraud Examiners (“ACFE”) published the 11th edition of its Global Study on Occupational Fraud and Abuse entitled Report to the Nations, examining both the costs and effects of occupational fraud. The study examined 2,504 reported cases of fraud from 125 countries, causing total losses of more than $3.6 billion, that were investigated between January 2018 and September 2019. This is just a fraction of the number of frauds committed each year against millions of businesses, government organizations, and nonprofits worldwide. The study estimates that the typical organization loses 5% of its revenues to fraud each year. The median loss caused by the occupational fraud (fraud by employees) cases in the study was $125,000. The average loss per case studied was $1,509,000, with 21% of cases causing losses of at least $1 million. All companies should be aware of the possibility of fraud, types of fraud, and methods of reducing the incidence of occupational fraud.

Common Types of Reported Fraud

Since the inception of the Report to the Nations in 1996, more than 18,000 cases of occupational fraud have been analyzed, and in each of the 11 studies conducted the ACFE has explored the mechanisms used by perpetrators to defraud their employers. In general, the studies have found that the schemes used by occupational fraudsters have stayed remarkably consistent. Among the various kinds of fraud that organizations might face, occupational fraud is likely the largest and most prevalent threat. At the highest level, there are three primary categories of occupational fraud:

- Asset Misappropriation;

- Corruption; and

- Financial Statement Fraud

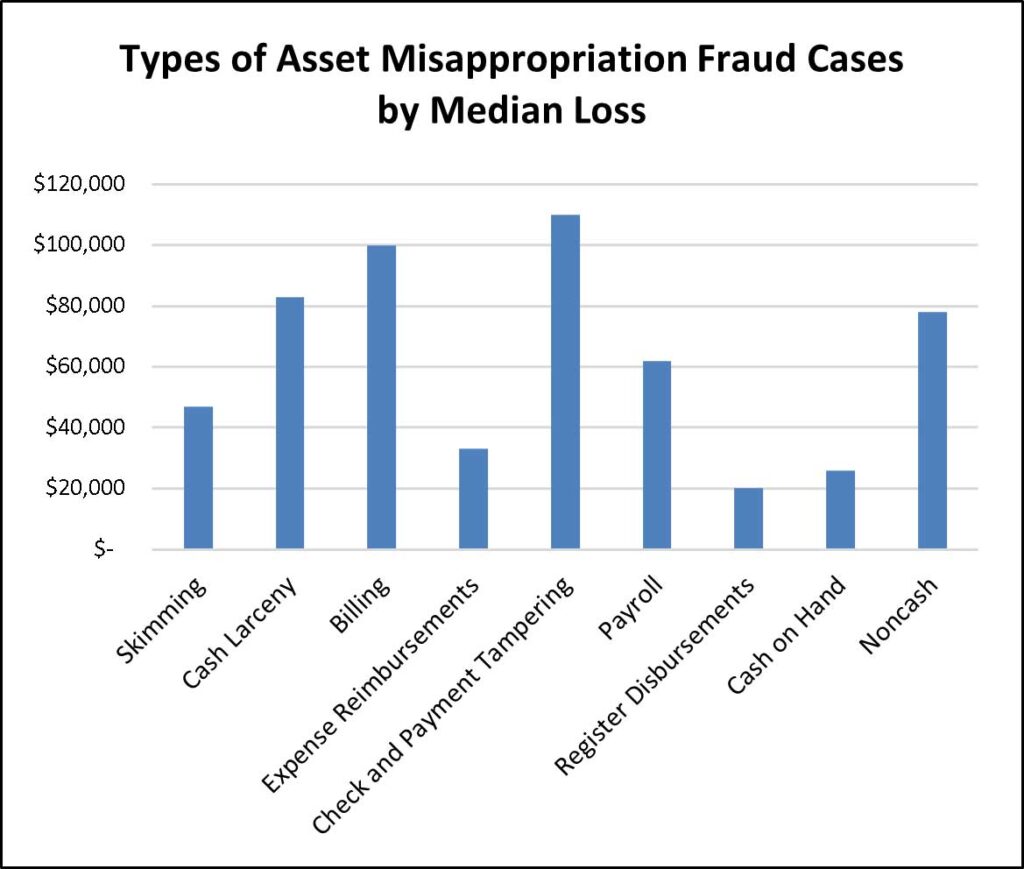

The most common (86% of all reported cases of fraud) and often most difficult type of fraud to identify is asset misappropriation; however, these schemes also tend to cause the lowest median loss at $100,000. This category of fraud includes nine major types of theft: skimming, cash larceny, billing schemes, payroll schemes, expense reimbursement schemes, check tampering, cash register disbursements, theft, and misuse of other assets. These types of fraud usually go on for extended periods of time before being detected and stopped. In the 2020 study, billing schemes were the most common form of asset misappropriation (20% of all cases), causing a high median loss ($100,000) with a median duration of 24 months, making this type of fraud a particularly significant risk. Noncash misappropriation (such as misuse, abuse, unconcealed misappropriations, transfer of assets, and proprietary information) had a median loss of $78,000 and the shortest period of time that the fraud went undetected, but even then the median duration was over a full year at 13 months. Not all fraud can be prevented, however quick detection of fraud is vital to protecting an organization from potential damage.

The next most common type of fraud is corruption with 43% of the Global Study cases involving some form of corruption (please note the totals add up to more than 100% because multiple fraud schemes often occur together). Corruption schemes – which include offenses such as bribery, conflicts of interest, and extortion – had a median loss of $200,000 and a median duration of 18 months. Top red flags in corruption cases are people who appear to be living beyond their means, are unusually close with vendors or customers, show signs of financial difficulties, or boast a “wheeler-dealer” attitude.

The least common and most costly category of fraud is financial statement fraud. This type of fraud includes fictitious revenues, misstated liabilities and expenses, and improper asset valuations. Given the level of access these types of fraud require, they are fortunately the least common. Only 10% of the Global Study includes these types of cases, but given the level of access and sophistication of perpetrators of this type of fraud, the median loss was a staggering $954,000.

Related: 2018 Report to the Nations: Global Fraud Study Summary

Concealment and Detection Methods

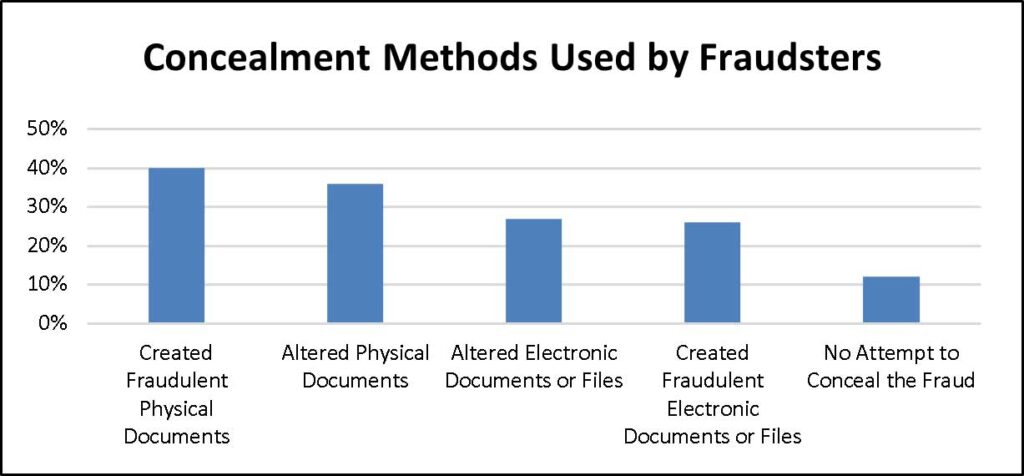

An act of fraud typically involves not only the commission of the scheme itself but also efforts to conceal the crime. Understanding the methods used to cover fraud can help organizations better design prevention mechanisms and detect the warning signs of fraud. The top 4 concealment methods used include creating fraudulent physical documents (40%), altering existing physical documents (36%), altering existing electronic documents or files (27%), and creating fraudulent electronic documents or files (26%). Again, take note that the percentages add up to more than 100% because most frauds involve more than one type of concealment method. Generally speaking, manager-level fraudsters are more likely to alter evidence while owners/executives are more likely to create or delete evidence.

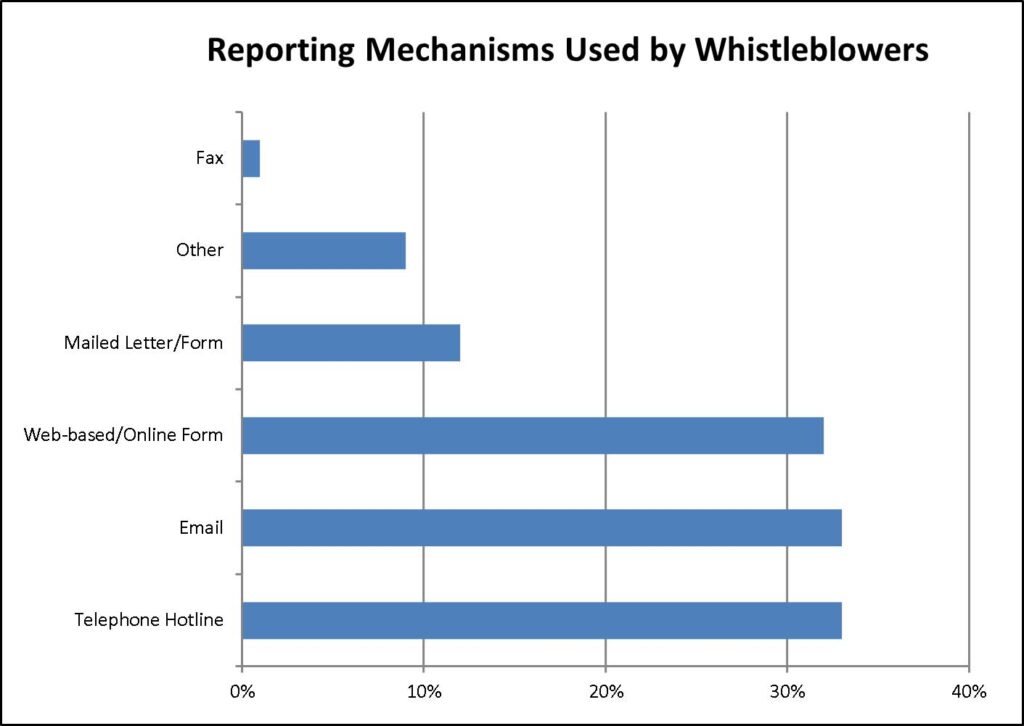

Despite the increasingly sophisticated fraud detection techniques available to organizations, tips are the most common detection method. In the study, more than 40% of cases were uncovered by tips, which is almost three times as many cases as the next-most-common detection method. In all fraud cases, half of the tips came from employees, while a substantial number of tips came from outside parties, including customers (22%), vendors (11%), and competitors (2%). The active cultivation of tips and complaints, such as the promotion of fraud hotlines, is often geared primarily toward employees. However, this data suggests organizations should consider promoting reporting mechanisms to outside parties. It’s also important to note that 15% of tips came from an anonymous source.

The presence of a hotline or other reporting mechanism affects how organizations detect fraud and the outcome of the case. Median losses were nearly doubled at organizations without hotlines and organizations with hotlines detect frauds more quickly and more often. It’s also important to note that fraud awareness training increases the likelihood of detection by the tip, and tips are more likely to be submitted through reporting mechanisms with training.

Given the scope of fraud and the potential for loss, how can organizations protect themselves and reduce the likelihood of fraud? The results of the 2020 Global Study show that some fraud detection methods are more effective than others in the sense that they correlate with lower fraud losses. Passive detection methods, meaning the fraud came to the victim’s attention through no effort of their own, including notification by police, by accident, or confession. Cases where the victim was notified by the police resulted in median losses of $900,000 with a median duration of 24 months. Active detection methods, meaning they involved a process or effort designed (at least in part) to proactively detect fraud, include document examination, management review, internal audit, account reconciliation, IT controls, and surveillance/monitoring. Frauds discovered through surveillance/monitoring had the lowest median loss of $44,000 and only had a median duration of 7 months. Detection methods such as external audits and tips can potentially be active or passive. What can be learned from this is that schemes discovered through active methods were shorter in duration and had lower median losses than those detected passively. Anti-fraud controls are tools that can lead to more effective detection of occupational fraud.

Occupational fraud is widespread from public companies to governmental units and nonprofits, from large corporations to small businesses. Fighting fraud takes a concerted effort across the organization and to be effective requires the implementation of multiple fraud reduction strategies. The use of targeted anti-fraud controls has increased over the last decade, and a lack of internal controls contributed to nearly one-third of frauds. No organization is immune from occupational fraud, and these crimes can originate from anywhere within the organization. Company owners, managers, and a Board of Directors may want to consider whether their organizations have taken the appropriate steps to detect and reduce the occurrence of fraud.

ABOUT WITHUM

Withum is a forward-thinking, technology-driven advisory and accounting firm, committed to helping clients in the hospitality industry be more profitable, efficient, and productive in the modern business landscape. For further information about Withum and its hospitality services team, contact Lena Combs (LCombs@Withum.com) at (407) 849-1569, or visit www.withum.com.